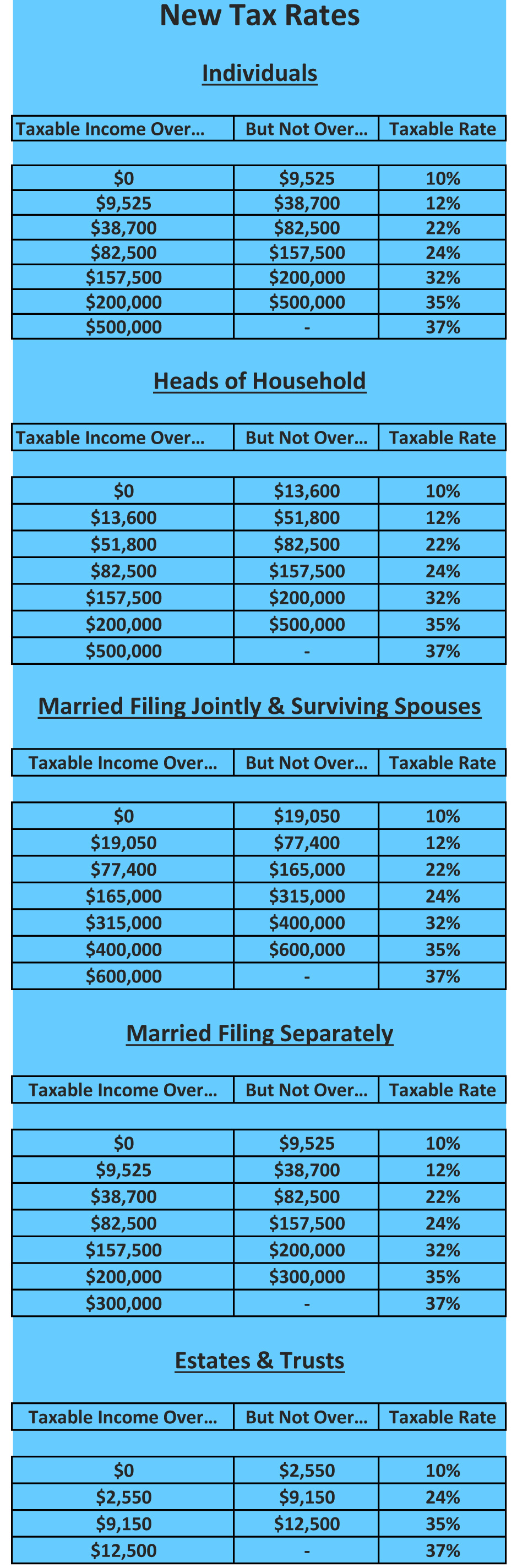

The new tax law was signed by Donald Trump in December. This is the most sweeping change in tax laws in over 30 years. While many of its provisions are clear-cut and easy to follow, some measures remain vague and will require additional study and interpretation. I will explain them as best as I can.

Income

Wages

Withholding tax tables for wage earners in 2018 and beyond will be revised to reflect the new income tax rates.

Alimony

Beginning in 2019 alimony will no longer be deductible by the paying spouse and will no longer be included in reportable income by the receiving spouse.

Capital Gains (or Losses)

Treatment of capital gains has not changed under the new tax law except that the 15% rate for married filing jointly taxpayers will begin at $77,200 of income, $51,700 for heads of household and $38,600 for individual taxpayers. The 20% rate begins at $479,000 for married filing jointly taxpayers, $452,400 for heads of household and $425,800 for individual taxpayers.

Pass-through Income

Pass-through income refers to income that is derived from a sole proprietorship, partnership or S-Corporation and does not include investment-related income. However, dividends derived from real estate investment trusts (REITs), qualified cooperative dividends and qualified publicly traded partnerships will be included in the pass-through income category. Beginning in 2018, those who earn their income from such entities will receive a 20% deduction against their net taxable income. In general, the deduction will be limited to 50% of W-2 wages paid to employees of these entities. One exception is that qualified business income will NOT include the reasonable compensation paid to S-Corporation shareholders. This provision is to prevent shareholders from maximizing distributions and minimizing their compensation in an effort to avoid payroll taxes. The deduction will be phased out for single taxpayers in specific service trades such as accounting, health, law, consulting, athletics, financial services and brokerage services with incomes above $157,500 or married people filing jointly above $315,000.

Business Taxes

Beginning in 2018 the tax rate for C-Corporations (not pass-through entities) has been reduced from a graduated rate of up to 35% down to a flat rate of 21%.

Simplified Accounting for Small Businesses

The new law raises the threshold up to $25 million in gross income below which C-Corporations may use the cash method of accounting, even if they have inventory. The law allows businesses with average gross incomes of $25 million or less for the three previous years to use the cash method.

Limits on Business Interest Deductions

Beginning in 2018 businesses will be limited to interest expense deductions equal to the amount of interest income received plus 30% of their adjusted taxable income. However, any excess may be carried forward for an unlimited period of time. Businesses with average gross incomes of $25 million or less will be exempt from this deduction limitation.

Changes to the Net Operating Loss Deduction

The 20-year limit for carrying net operating losses forward has been repealed. Beginning in 2018 NOL’s created and carried forward to future years will not be permitted to offset more than 80% of their taxable income calculated before the use of the NOL deduction.

Section 1031 Like-Kind Exchanges

Like-kind exchanges of property completed in 2018 or after will be limited to real property that is held in a trade or business or for investment. This will impact those that are in the business of flipping properties.

Business Depreciation Deductions

Bonus Depreciation

From 2018 through 2022 businesses will be allowed to deduct 100% of the eligible business property placed in service. However, the allowable bonus depreciation amounts will be phased down to 80% of allowable property in 2023, 60% in 2024, 40% in 2025 and 20% in 2026.

Section 179 Expense Election

The new tax law has increased the maximum amount businesses can claim for the Section 179 expense election for new assets purchased to $1 million per year.

Exemption for FICA and FUTA Taxes -Schedule C Hiring of Children

Beginning in 2018 sole proprietorships can exempt up to $12,000 from FICA and FUTA taxes on wages paid to their children.

Deductions

Itemized Deductions

Medical Expenses

For tax years 2017 and 2018 all taxpayers with qualified medical expense deductions will be allowed to claim the amount that exceeds 7 1/2% of adjusted gross income. However, in 2019 and future years the 7 1/2% floor rises back up to 10% of adjusted gross income for taxpayers under the age of 65, as it was during the past several years. It’s unclear why Congress chose to offer this break for just two tax years.

Mortgage Interest

The interest expense deduction for home equity lines of credit has been repealed through 2025 unless the proceeds are used for home improvements or renovations. Additionally, the basis for deducting primary mortgage interest has been reduced from mortgage debt of $1 million down to $750,000.

State and Local Taxes

Beginning in 2018 married couples filing jointly will be limited to deducting $10,000 for state and local taxes, such as W-2 withholdings, estimated tax payments, real estate taxes, sales taxes, vehicle registration fees, etc. The maximum deduction for married couples filing separately will be $5,000. This will clearly have a negative impact on residents of such highly-taxed states as California, New York, New Jersey and Massachusetts.

Charitable Contributions

One bright spot within the new tax legislation increases the limit on charitable contributions from 50% of adjusted gross income to 60%.

Miscellaneous Itemized Deductions

The following miscellaneous itemized deductions previously limited to the amount above 2% of adjusted gross income have been repealed entirely:

- estate taxes

- gambling losses

- hobby expenses

- investment advisory fees

- professional subscriptions

- safe deposit box fees

- tax preparation fees

- uniforms and protective clothing

- union and professional dues

- work tools

From 2018 through 2025 the moving expense deduction is repealed for all taxpayers other than members of the armed forces on active duty.

Standard Mileage Rate

The standard mileage rate for 2018 has been increased to 54½ cents per mile for business mileage, 18 cents per mile for medical travel and 14 cents per mile for service to charitable organizations.

Standard Deduction

Beginning in 2018 the standard deduction has been raised to $12,000 for individuals, $18,000 for heads of household and $24,000 for married couples filing jointly. Elderly (age 65 and over) and blind taxpayers may claim an additional deduction of $1,550 for singles and heads of household and $1,550 per spouse for married couples filing jointly.

Personal Exemptions

The new tax law has repealed all personal exemptions from includible income.

Tax Credits

Child Tax Credit

Beginning in 2018 the child tax credit has been increased to $2,000 for each qualifying child. The maximum refundable credit is $1,400. The tax credit has been expanded to include qualifying dependents who are not qualifying children. The phase-out amount for the credit has been increased to $400,000 for married filing jointly taxpayers and $200,000 for all other taxpayers.

Alternative Minimum Tax

From 2018 through 2025 the phase-out amount for the alternative minimum tax (AMT) is increased to $109,400 for married filing jointly taxpayers, $54,700 for married filing separately and $70,300 for heads of household and single taxpayers. The exemption for the alternative minimum tax will be phased out at $500,000 for single taxpayers and $1 million for married filing joint taxpayers. Because miscellaneous itemized deductions and deductions for state and local taxes were among the biggest tax-preferenced items triggering the alternative minimum tax in the past and have been eliminated under the new tax law, many taxpayers will no longer be subject to the tax.

Estate, Gift and Generation-Skipping Transfer Taxes

Beginning in 2018 the exemption for these taxes has been doubled from $5.6 million to $11.2 million and will be indexed to inflation for entities after 2011.

Affordable Care Act

The new tax law eliminates the individual mandate that required taxpayers to obtain minimal health insurance coverage or face penalties. However, the additional 3.8% Medicare tax remains in place for investment income received by high-income taxpayers, which essentially funds the Affordable Care Act.